Banks in the US are Quietly Panicking: Traditional Money Steps Up to Fix Things.

First segment by James Hickman. Second segment by Jon Forrest Little

January 16, 2025

Bank of America released its quarterly earnings report this morning, bright and early at 6:45am. And according to their newest financial statements, the bank is currently sitting on a whopping $112 BILLION in net unrealized bond losses.

To say this is atrocious would be a massive understatement. Yet Bank of America had the audacity to say that their “balance sheet remained strong” throughout 2024.

What a hilarious fiction. Do they seriously think that no one will notice $112 billion in bond losses— nearly FIFTY SEVEN PERCENT of the bank’s tangible common equity? How stupid do they think people are?

Bank of America is the poster child for the looming problems in the US banking system; we’ve talked about this in the past... but just to refresh your memory, this is also how Silicon Valley Bank went bust in 2023.

Back during the pandemic when interest rates were essentially zero, Silicon Valley Bank invested over $100 billion of its customers’ money in US government bonds— supposedly the safest asset in the world. What could possibly go wrong?

Well, it turns out that even US government bonds are volatile and risky. And as interest rates began to rise throughout 2022, the value of Silicon Valley Bank’s bond portfolio plummeted.

This is the cardinal #1 concept to understand about bonds: if you buy a bunch of bonds, then interest rates rise, the value of the bonds that you already purchased goes down.

In the case of Silicon Valley Bank, they loaded up on bonds when rates were 0%. Then interest rates surged to 4% in a very short period of time in 2022. A short time later, the bank’s bond wiped out its entire capital reserves, rendering Silicon Valley Bank insolvent.

Bank of America did the same thing: they bought up hundreds of billions of dollars worth of federal bonds during the pandemic when interest rates were at all-time lows, i.e. when bond prices were at all-time highs.

Interest rates are now significantly higher than they were in 2020/2021. And as a result, the value of Bank of America’s bonds has plummeted by a whopping $112 billion.

Again, $112 is an extremely significant number because Bank of America’s average “tangible common shareholder equity”, which is a critical measure of its capital and safety, is only $197 billion.

So in other words, the bond losses constitute almost 57% of that essential capital reserve.

This is not a problem isolated to Bank of America— their losses just happen to be the biggest.

Back in December, the FDIC estimated total unrealized bond losses across the entire US banking sector to be roughly half a trillion dollars.

Given that bond yields have risen sharply since then, the unrealized bond losses across America’s banks have only become worse.

There are some banks, in fact, who like SVB, have been rendered insolvent by their bond losses. And others, like Bank of America, are sitting on enormous unrealized losses.

(If you want to see for yourself, the College of Business at Florida Atlantic University has put together something called “The Banking Initiative” which tracks every bank’s exposure to unrealized bond losses.)

To be fair, there are plenty of banks that are in good shape. I’m personally not a fan of big banks— they typically have pitiful service and bureaucracy, or wanton fraud in the case of Wells Fargo.

But it’s important to be intellectually honest and acknowledge that JP Morgan has a solid balance sheet. And there are a number of others as well who are not exposed to the steep losses in the Treasury market.

Yet it’s clear that dozens and dozens of banks in the US, big and small, are quietly panicking... and praying for lower interest rates.

Lower interest rates would solve the problem for them by increasing the value of their bond portfolios, reducing the unrealized losses, and forestalling a capital crunch or even insolvency.

The Federal Reserve is keenly aware of this problem. That’s one of the reasons why the Fed has been trying to lower interest rates for the past several months.

In fact, the Fed has cut its benchmark policy rate three times, in each of its last three meetings, even though inflation is still on the rise.

Unfortunately for the Fed, and for these troubled banks, the bond market isn’t listening.

In September, when the Fed began cutting rates, the yield on the 10-year Treasury was as low as 3.59%. Since then, even though the Fed has tried to cut rates three times, bond yields have surged, reaching a high of 4.89% just a few days ago.

So it’s obvious that the Fed has completely lost control of the bond market.

There was a time that the Fed was able to move markets with a few well placed words in an otherwise boring speech. Alan Greenspan, Fed chairman back in the 1990s, was legendary for his cryptic messaging which could send both stock and bond markets swooning.

But it’s clear the Fed just doesn’t have the same pull that it once did. Even though they are actively cutting their own internal policy rate, the market is simply not following along.

And that’s a huge problem for these troubled banks.

The key culprit here of course is the federal government. Every year the government runs a multi-trillion dollar deficit, and obviously in order to finance that deficit, the Treasury Department has to issue trillions of dollars worth of new bonds.

Surging bond yields are simply an issue of supply and demand. The supply of government debt keeps increasing at an astonishing rate thanks to irresponsible reckless spending.

Investment demand from individuals, businesses, foreign governments, foreign central banks, etc. to buy US Treasurys, on the other hand, is waning. Especially from foreigners.

The natural result of this disparity between supply and demand is that bond yields keep rising. And that causes mortgage rates, credit card rates, etc. to rise as well.

Realistically there’s only two ways that interest rates will fall.

One, the Fed will have to directly intervene in the bond market. This means they will “print” trillions of dollars, then use that money to buy government bonds.

This would create artificial demand for Treasurys and bring interest rates down. They’ve done it before— after the 2008 financial crisis and again after COVID.

They call it quantitative easing. And unfortunately, as the world discovered after 2021, quantitative easing creates a lot of inflation.

The second option is a lot more difficult. That is for politicians in Washington DC to summon the courage and the will to make very difficult decisions and cut spending.

Combined with a regulatory overhaul and a new embrace of capitalism— which would seriously boost economic growth and federal tax revenue— the budget deficit and the national debt could actually be brought under control.

In other words, the government could reduce the supply of Treasurys. And that would naturally bring interest rates down.

The latter option is clearly the better one because it creates the most prosperity for everybody.

But if they don’t get it right, inflation is the obvious outcome.

And that’s the primary reason why it continues to make so much sense to own real assets— as a hedge against the potential inflation to come.

end of first segment by James Hickman, co-founder of SchiffSovereign

The Following Segment by Silver Academy’s Jon Forrest Little

Los Angeles Faces Financial Apocalypse: 70% Insurance Exodus Triggers Unprecedented Banking Crisis, Crushing the System from Both Ends

Before we get to the news on how the Fire in LA will trigger local and regional bank failures, let’s first understand how “screwed up” our banking sector is.

In the intricate world of finance, a startling truth lurks beneath the surface: banks possess the extraordinary ability to create money out of nothing. This revelation challenges our fundamental understanding of money and the banking system, exposing a reality that few comprehend but impacts us all.

For centuries, we've been led to believe that banks are mere intermediaries, collecting deposits from savers and lending them out to borrowers. However, the truth is far more intricate and fascinating than this simplistic view.

Banks operate on a much more complex and powerful level, wielding the ability to expand the money supply with a few keystrokes.

The process is deceptively simple. When a bank approves a loan, it doesn't reach into a vault of existing deposits. Instead, it creates new money by crediting the borrower's account with the loan amount. This digital entry becomes real money, spendable and transferable, without any physical cash changing hands.

This money creation process, a theoretical concept, is not just a matter of academic interest. It's a practical reality confirmed through empirical research. In a groundbreaking study, researchers observed the internal workings of a bank during a real loan transaction, shedding light on the actual mechanisms at play.

The results were clear:

As the loan was issued

No existing deposits were drawn down

and no reserves were touched.

The money was created

Expanding the bank's balance sheet and the overall money supply.

The legal framework supporting this system is equally surprising. What we colloquially call "bank deposits" are, in fact, not deposits at all.

When we "deposit" money in a bank, we're actually lending it to the bank. The bank becomes the owner of the funds, and we become creditors with a claim on the bank. This legal sleight of hand allows banks to use our "deposits" as they see fit, including as a basis for further money creation.

Similarly, when banks "lend" money, they're not actually lending in the traditional sense. Instead, they're purchasing securities – the promissory notes or loan contracts that borrowers sign. The "money" that appears in a borrower's account is simply the bank's liability, created at the moment of the loan.

This system of money creation has profound implications for our economy and society. It explains why banks hold such a central and powerful position in our financial system. They are not just intermediaries but the very creators of our money supply. This power gives them enormous influence over economic cycles, inflation, and wealth distribution.

Moreover, this reality challenges many conventional economic theories and policies. For instance, the idea that banks need deposits or reserves to lend is essentially a myth.

Banks create money first and look for reserves later if necessary. This turns the traditional view of banking on its head and calls many current monetary policies into question.

The implications extend to financial stability as well. If banks can create money at will, what stops them from doing so excessively?

The answer lies in regulatory constraints, market forces, and the banks' own risk assessments. However, as we've seen in past financial crises, these checks can fail, leading to credit bubbles and economic instability.

Understanding this reality of money creation is crucial for policymakers, economists, and the public alike. It shifts the focus of monetary policy from controlling the money supply through central bank operations to regulating and guiding the credit creation activities of commercial banks.

Central banks play a crucial role in this, setting reserve requirements at ZERO and influencing interest rates to manage the money supply and ensure financial stability.

This knowledge is empowering for the average citizen. It helps us understand the true nature of our financial system and the responsibilities that come with it. It challenges us to question the current structure and demands greater transparency and accountability from our financial institutions.

Critics might argue that this view of banking is too simplistic or that it overstates banks' power.

However, the empirical evidence and legal framework support this understanding of money creation. It's not a conspiracy theory but a documented reality of our financial system.

As we grapple with ongoing economic challenges and seek to build a more stable and equitable financial system, acknowledging and understanding the true nature of money creation is essential. It's time to move beyond the myths and misconceptions about banking and face the reality of how our monetary system honestly operates.

Our banking system urgently requires a comprehensive overhaul.

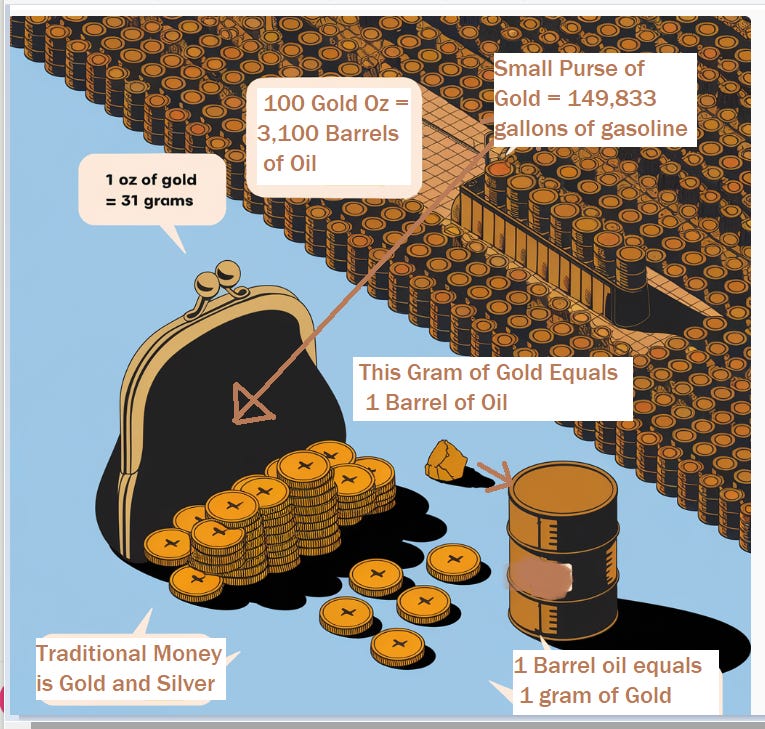

What does Traditional Money Look like?

It's imperative that we advocate for and cultivate a significantly enhanced public understanding of money—one rooted in transparency and accountability.

This newsletter aims to clarify often misunderstood terms like "hard money" or "sound money" by reframing them as "traditional money," which we define exclusively as silver and gold.

An ounce of Gold is about 31 grams.

A barrel of oil is worth 1 gram of gold

A small purse can hold 100 gold one ounce coins

Meaning that same small purse can purchase 3,110 barrels of oil

Good luck doing that with fiat debt notes

By recognizing the power of banks to create money, we can work towards a more transparent, stable, and fair financial system that serves the needs of society as a whole.

The truth about banks' money creation is a wake-up call. It invites us to engage more critically with our financial system and demand the changes necessary for a more robust and equitable economy.

As we move forward, let this knowledge guide us toward a future where the power of money creation is understood, respected, and harnessed for the common good.

end of segment

Please Chip in to support the Silver Squeeze

While independent media outlets face unprecedented challenges, The Silver Academy stands resilient. We are the only silver-focused newsletter in the USA delivering 12+ weekly articles on groundbreaking silver stories.

From Silver solid-state batteries to Federal Reserve manipulations, our investigative journalism shines a light on critical issues.

In an era where many independent voices are struggling to survive, help us grow stronger. We need your help to continue our mission.

Big Tech's algorithm changes have throttled traffic to news sites but we are growing (between the Pickaxe and Silver Academy we have over 70,000 daily readers) making Silver specialized reporting like ours more crucial than ever.

Your support ensures we remain a beacon of truth in the silver market. Invest in real, independent journalism today.