UBS states "This is the Year of Silver"

Also, market distortions in US housing and S&P 500 will usher stampede into Gold and Silver investing.

Op-Ed by Bernadette Driscoll

The current state of the U.S. housing market is a glaring contradiction, revealing deep-seated distortions that raise serious concerns about the trouble in our economy.

As housing prices have skyrocketed by over 50% since May 2020, and the S&P 500 has more than doubled, an unsettling question arises: how can asset prices continue to rise amid a backdrop of plummeting mortgage demand and unprecedented housing unaffordability?

Jon Forrest Little offers a compelling perspective on housing prices:

"Take a look around your house at the basics. The most expensive components—kitchen and bath fixtures, windows, flooring, plumbing, electrical systems, and exterior cladding—haven't improved over time. In fact, they've all depreciated. The costliest aspect of a home is labor, which has actually become cheaper when adjusted for inflation. This revelation doesn't indicate that house prices are skyrocketing; rather, it exposes the alarming rate at which the dollar is losing its value."

The Housing Market Freeze

Mortgage demand in the United States has plunged to its lowest level since 1995, with applications down a staggering 63% from their peak less than four years ago.

Homebuyers are effectively giving up, as the annual income required to purchase a median-value home has soared to a record $109,564, which is nearly $26,133 more than the median household income of $83,431.

The annual income needed to buy the median-value home in the US risen to a record $109,564. This value has DOUBLED in just 4 years.

This gap is not only alarming but also represents the largest disparity ever recorded between necessary income and actual earnings for homebuyers. In comparison, during the 2006 housing bubble, this difference was around $10,000—a stark reminder of how far we have fallen into an affordability crisis.

Historical Context and Current Trends

In June 2024, the housing market made headlines for another troubling reason: it became cheaper to buy new homes than existing ones—a reversal of traditional market dynamics.

The median price for new homes was $417,400, while existing homes averaged $419,300. This anomaly raises red flags about the health of the market; when new construction is less expensive than older properties, it signals a fundamental disconnect between supply and demand.

Moreover, existing home sales have reached their lowest levels since 1995, with only about 4.04 million transactions in 2024—numbers that fall below those seen during the financial crisis of 2008. High interest rates combined with record prices have created a lethal cocktail that has effectively frozen the market. The median age of homebuyers has increased significantly to 49 years, indicating that younger generations are being systematically locked out of homeownership.

The Distortion of Asset Prices

Despite these alarming trends in housing, asset prices continue to ascend at an astonishing rate. The S&P 500's performance, driven largely by a handful of tech giants dubbed the "Magnificent Seven," has defied gravity—rising over 100% since the pandemic began. This surge is particularly perplexing given that many of these companies do not contribute to traditional manufacturing jobs in America. Instead, they rely on global supply chains that often exploit labor in countries with lax regulations.

This disconnect between asset prices and real economic conditions raises serious questions about market integrity.

With housing prices at unsustainable levels, savvy investors are redirecting capital to gold and silver, markets that still offer meaningful entry points and robust long-term appreciation potential.

While central banks around the world hoard gold as a hedge against economic instability, American consumers should be turning towards precious metals as a refuge from an increasingly volatile market. We have written extensively that Thailand, Vietnam, India, China and Russia Generation Z is actively purchasing gold and silver.

In India women hold vast gold reserves—amounting to 24,000 tons—that dwarf the combined holdings of the top 5 nations.

The Future: A Call to Action

As we navigate this tumultuous economic landscape, it is crucial for Americans to remain vigilant about global financial trends. Observing what central banks are doing with gold reserves can provide insights into future economic stability.

Likewise, understanding the behaviors of younger generations in emerging markets may offer clues about shifting investment strategies.

The current situation demands urgent action from policymakers to address our troubling economy beginning with bringing manufacturing back to USA.

Without leadership, we risk perpetuating a cycle of wealth concentration among cash buyers while younger generations remain locked out of homeownership—a scenario that could lead to long-term economic stagnation.

In conclusion, as we stand at this crossroads in 2025, it is imperative that we confront these distortions head-on.

The juxtaposition of soaring asset prices against a backdrop of stagnant wages and declining home sales cannot be ignored. We must “get back to work” here in America by reinvigorating our manufacturing base if we hope to build a resilient economy for future generations.

end of segment

UBS: Silver should outperform

They forecast of a 25% return for silver, with prices trading in a USD $36-$38/oz range,

Silver prices lagged gold prices in 2024. This is not unusual despite silver having a beta to gold price changes in the range of 1-2 times. Over the last 50 years, when gold prices rose, silver outperformed only half the time. But what happens after silver underperformed gold in those years, like in 2024? Over the last 50 years, silver had a positive absolute performance 67% of the time in the following year.

Moreover, for those years, the annual mean for silver price changes was 21% on average—versus a mean of 3% over the full observation window.

History is not a guarantee for future returns, especially given the multiple uncertainties associated with Trump’s proposed policies. Nevertheless, it’s an interesting starting point when considering silver’s return potential in 2025. Our forecast of a 25% return for silver, with prices trading in a USD 36-38/oz range, is quite lofty; consensus estimates (Bloomberg) stand at around USD 32-33/oz for 4Q25.

We see three drivers that should push prices up. First, the top-down narrative should be positive, as we expect US interest rates to be cut more than what’s currently implied by markets for this year. This should also lead to a moderation in USD strength. Second, we expect manufacturing to recover in the developed world.

Lower interest rates should help revive capex and industrial activity, translate into robust industrial application demand growth, and ultimately lead to greater investor interest in silver (the more important driver).

Lastly, we still expect mine supply to be constrained even though prices have jumped. Secondary silver supply, driven by zinc and copper prices, should remain challenged, at least in 1H25.

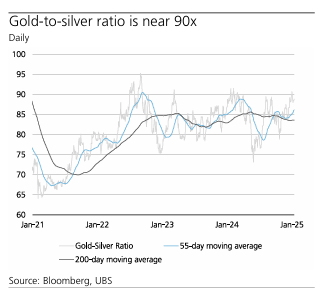

Altogether, we see a positive backdrop for silver prices with the gold-silver ratio potentially reaching 75x. But there are risks to our view, the biggest of which relates to higher US interest rates. The negative impact of higher rates on risk assets, including silver, would likely be significant.

As we wrote yesterday the average over past 30 years is 65 to 1

whereas historical is around 15-1

Taken out of ground ratio is 8 ounces of silver for every ounce of gold

Above ground inventories (about 7 billion ounces of gold and about 3.75 billion ounces of silver)

Yes you read that correctly there is more gold above ground than Silver

We are in year 5 of structural silver deficit with silver mining declining

2025 projected mining under 830,000,000 ounces

No new silver discoveries

Mexico the #1 supplier of Silver signaling Nationalizing

RE Gold to Silver Ratio: Even a move to 65 to 1 would be massive.

end of segment

Please Chip in to support the Silver Squeeze

While independent media outlets face unprecedented challenges, The Silver Academy stands resilient. We are the only silver-focused newsletter in the USA delivering 12+ weekly articles on groundbreaking silver stories.

From Silver solid-state batteries to Federal Reserve manipulations, our investigative journalism shines a light on critical issues.

In an era where many independent voices are struggling to survive, help us grow stronger. We need your help to continue our mission.

Big Tech's algorithm changes have throttled traffic to news sites but we are growing (between the Pickaxe and Silver Academy we have over 70,000 daily readers) making Silver specialized reporting like ours more crucial than ever.

Your support ensures we remain a beacon of truth in the silver market. Invest in real, independent journalism today.