Countdown to Basel III. Bullish Outlook For Gold and Silver

Gold will be upgraded from a Tier 3 to a Tier 1 asset with a 0% risk weighting, similar to cash and government bonds.

Implementation of Basel III and Implications for Gold

Basel III, a regulatory framework designed to enhance banking stability, will be implemented in the U.S. starting July 1, 2025. This reform strengthens bank capital requirements, limits leverage, and increases liquidity standards to mitigate financial risks. Its implementation is expected to have significant implications across various sectors, including the gold market.

Gold Market Implications

Reclassification of Gold:

Gold will be upgraded from a Tier 3 to a Tier 1 asset with a 0% risk weighting, similar to cash and government bonds.

Paper Gold RISKY

Unallocated gold, on the other hand, will be classified as a risky asset. This includes all 'paper' gold, such as futures contracts, ETFs, and other securities that have gold as an underlying but not allocated amount.Previously, banks needed to hold more capital against gold holdings (Tier 3 classification). The upgrade reduces this requirement, making gold a more attractive reserve asset for banks.

Unallocated Gold:

This bears repeating. Unallocated gold (e.g., futures contracts, ETFs Paper Gold) will be classified as a risky asset under Basel III.

This regulation aims to limit the issuance of securities backed by non-existent gold reserves.

Impact on Physical Gold:

Basel III regulations endorse the value of physical gold.

As banks transition from unallocated to allocated gold holdings, demand for physical gold is expected to rise, potentially increasing its value.

Derivatives and Clearing:

Basel III encourages shifting derivatives exposure toward centrally cleared counterparties (e.g., COMEX and NYMEX) rather than over-the-counter (OTC) trading platforms like LBMA.

Macro Trends

Global Debt and Money Supply:

Global debt has surged to $318 trillion (300% of global GDP), up from $175 trillion (200% of GDP) a decade ago.

Money supply has increased by $80 trillion since the Global Financial Crisis, reaching $107 trillion.

Derivatives Market:

Global OTC notional derivatives stand at an all-time high of $730 trillion (700% of global GDP), compared to $550 trillion five years ago.

Gold Price Correlation:

Historically, gold prices have shown a strong negative correlation (~-0.90) with U.S. TIPS yields.

Based on this correlation, gold should be trading at ~$3,120/oz compared to its current price of $2,977/oz.

Central Bank Demand:

Central banks have been net buyers of gold for 15 consecutive years.

In 2024, demand exceeded 1,000 tons for the third consecutive year, driven by emerging markets like Poland, China, and India.

COMEX Gold Contracts:

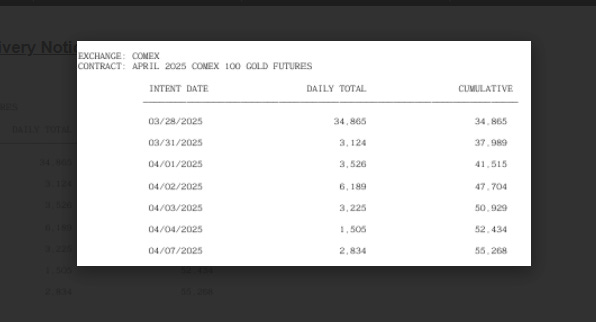

April 2025 saw record demand for delivery on COMEX contracts, with 5.28 million ounces standing for delivery—the third-highest monthly figure ever recorded.

Inflation and Hard Assets:

Persistent global inflation is driving investors toward hard assets like gold due to its historical role as a safe haven.

Gold Industry Challenges

Depleting Reserves:

Gold producers are depleting existing reserves while facing declining asset quality.

Over the past decade:

Reserve grades have fallen by 55% (to an average of 1.15 g/t).

Top 10 producers' reserves have decreased by 33%.

Exploration Underinvestment:

Exploration budgets have declined despite rising gold prices.

No major new discoveries have been made recently, creating a looming "supply cliff."

Gold Equities

Investment Opportunities:

Mining companies offer high-beta exposure to rising gold prices but remain undervalued.

An M&A cycle is anticipated as producers seek to replenish depleting reserves.

Fund Flows into ETFs:

Total assets in gold/silver bullion ETFs rose by $46 billion in 2025 (to $270 billion), while precious metal equities ETFs increased by only $3 billion (to $28.5 billion).

The ratio of bullion ETF assets to equities ETF assets is at an elevated level of 9.47:1—well above the five-year average of 7.50:1.

Net Flows Comparison:

Bullion ETFs saw net inflows of $7 billion year-to-date.

Precious metal equities ETFs experienced net outflows of $1.8 billion.

This comprehensive analysis highlights Basel III's transformative impact on the financial system and its potential to reshape the dynamics of the gold market and related industries.

Figure 1 – US Banks’ Centrally Cleared Derivative Contracts as a % of Total Derivative Contracts (OCC report)

Figure 2 – Global Money Supply vs Gold Price

Figure 3 – Historical Regression - US 2-year TIPS Yield vs Gold Price

Figure 4 - Global 2024 Exploration Budgets per Metal

Figure 5 - Total Au & Ag Bullion ETF Assets (blue line) vs Total Precious Metal Equities ETF Assets (white line)

Figure 6 – COMEX Gold Delivery Notices – April 2025