Jon Forrest Little Bank Funds Frozen: Bank Teller Limits Withdrawal.

Jon Forrest Little Bank Funds Frozen: Bank Teller Limits Withdrawal.

Get Ready for My Experience to be Your Reality Too.

As a precious metals news reporter, I've been urgently covering topics related to systemic and geopolitical risk. This style of reporting can be interpreted as “negative” but there is no exaggerating here.

If people trusted our political and economic system I would expect gold and silver to drop in price so the opposite is also true. Gold and silver will soar as we see dwindling trust in our financial and political institutions.

-War spending (a staggering 251 wars and conflicts since 1991 verified by Congress's own records)

-Insider trading by members of Congress ( I was one of the first to report that the US is no longer a 'Democracy' (voice of people) but transitioned to a 'Plutocracy/Aristocracy hybrid' (ruled by an elite few) but is now a 'Kleptocracy' ( Ruling class theft out in the open through war profiteering, Seigniorage, excessive taxation, and inflation tax)

-Seigniorage, in simpler terms, is the profit made by the government when it creates money. It's the difference between the value of the money and the cost to produce and distribute it.

-The zero reserve requirement, within the fractional reserve banking system, is a policy that allows banks to lend out all of their deposits, without keeping any in reserve. This can lead to financial instability and is a key factor in the banking system's vulnerability to crises.

-The fact that when you deposit money in a US bank, it is no longer your money but instead an unsecured loan to the bank

-How Banks are technically insolvent. (more on this below)

-The commercial real estate crash, a significant downturn in the commercial property market, will be way more devastating than the 2008 subprime crash, a housing market crisis.

-The BIS, ECB, Federal Reserve, and Central Banks worldwide are developing a tokenized CBDC system (complete with biometric authentication / facial recognition / the digital ID)

-In October, at a summit in Kazan, details of a single BRICS currency will be revealed, which will put an end to the dollar's 80-year hegemony in the world.

Slowly but surely, the BRICS countries are getting closer to creating an alternative to the dollar

The creation of a single BRICS currency enters a decisive phase

The BRICS countries are implementing a three-stage plan to create an alternative international currency. According to preliminary information, they plan to adopt a gold standard, develop a single payment system with the introduction of new technologies, and ensure the distribution of central bank digital currencies. The implementation of these plans will create a new reality in the global economy, where the American currency has reigned supreme since the Bretton Woods Conference.

The Dystopian World Financial Tracking is Already here

A federal law, the USA Patriot Act of 2001, requires all US banks to follow strict Know Your Customer (KYC) rules. These KYC rules include the Customer Identification Program (CIP) and Customer Due Diligence (CDD).

Governments use digital ID systems to increase surveillance of their citizens.

Digital IDs enable the tracking of individuals' activities and transactions.

The irony is that the excuse offered by the Ruling class is that this surveillance is for our protection, and it fights Money Laundering when no one in the World is better at Money Laundering than the Political Class.

This trend always starts with air travel and driver's licenses. (sort of like a hall pass, if you want the freedom to go to the bathroom, you better have your hall pass)

Similar to a vaccine card, show us your papers if you want to travel.

This leads to a total loss of privacy and autonomy.

This concern is particularly pronounced in countries with a history of government overreach.

Digital IDs and Digital payments (tokenized by FedNow) track your spending

BIS president recently stated, "We need to know how and by whom every 100-dollar bill is spent."

WTF? How did this not make headlines in the NY Times or WaPo?

Track your spending

Track your movement

Freeze your Funds

Debit your account for Fines, Penalties and Taxes

Funds will also expire, thus discouraging savings

Public Distrust

Public resistance to digital ID systems is often rooted in a general distrust of centralized economic and political power. For example, in the US, there is significant opposition to the idea of a national identity card, which parallels the resistance to digital currencies and digital ID systems due to fears of government surveillance and control.

Our friend and colleague Peter Spina Speaks Truth-to-Power

Jon Little's funds are frozen.

Recently, while I was in New Mexico (visiting my mom who lives in the 4 Corners area), my bank decided to put fraud alerts on both my business and personal accounts, causing a significant disruption to my daily life.

When I called the 1-800 number on the back of my bank card, the customer service rep stated they needed to verify me.

Typically, I have no concern over being verified (usually, one confirms their social security number or amount of last deposit or some security question like the name of your first pet or mother's maiden name)

But they came at me with this new criterion, which they explained is "for my protection."

The One-time text code:

A one-time text code is just that—a text that is supposed to hit your mobile phone, and then you reply with the code.

However, I did not receive a code. The banker's customer service department stated that since I didn't supply them with the code, they would not remove the fraud alert from my card.

The bank "flagged the fraud" from a purchase I routinely make 3 to 4 times per month originating from an SMS texting platform (a service we use weekly called Textmagic). The Silver Academy sends out articles via SMS, just like it does via email.

The bank stated that there is a high volume of fraud and that Know Your Customer and Anti Money Laundering protocols are necessary, justifying why they are going with their new one-time text protocol. It wasn’t in place the month before.

I explained that many Americans may not want to combine their phone numbers with banking (See the list above of privacy concerns )

I was with my mother and told her this is a new obstacle to make it harder to withdraw money or use your card for a purchase (which is also like taking money out of their clutches)

I kept on pleading with them to come up with another way for me to be verified because their one-time text code was not reaching my phone.

I stated that since I was traveling in remote New Mexico. It sounded absurd that I had to explain the need to locate subsistence (like food, water, and gas for my travels). The bank could not be more dismissive of how I would access my money.

They stated I needed to go into my branch. I said I was in New Mexico (6-hour plane trip from my branch, 3-day car travel time, 4-day bus travel time, 5-day train travel time, etc.)

The story took a turn for the worse, becoming more bizarre, inconvenient, and downright unpleasant.

When I finally arrived at my home bank branch, they said they could not reset my phone number for verification because it was not linked to the three credit reporting agencies: Equifax, Experian, and TransUnion.

Again, this was beyond horrible. It was inconvenient, unpleasant, and almost like a self-fulfilling prophecy, as I have been writing and warning our readers that banks will be conjuring up all sorts of obstacles between MY MONEY and ME (Precisely because they are illiquid)

I have been writing this story, but now I was the story.

The incident was so surreal. But apart from living a nightmare, I felt compelled to create a paper trail. The experience was so unnerving, unsettling, and disturbing that I wrote a letter to the bank manager (with some help from AI). The letter is below

Michael,

It's concerning that your bank is relying solely on a one-time text code generated from a credit bureau to verify your customer’s identity, as this method excludes individuals without phones or those whose numbers are not registered with credit bureaus.

This approach raises accessibility issues and prevents legitimate account holders from accessing funds. As I told you in person this just happened to me while traveling in New Mexico. It is on the road when I need the bank to help out (vs when Im at home and i can step into a branch office and visit with a manager like yourself.)

Here are some critical concerns regarding this One time text code verification method:

Traditional verification methods like social security numbers, mother's maiden name, or recent deposit amounts are more inclusive and should still be accepted as valid forms of identification.

Relying exclusively on a one-time text code from a credit bureau discriminates against individuals without mobile phones or those whose numbers are not associated with credit bureaus, such as elderly individuals, maybe low-income households, or those with limited credit histories.

Why punish people who don’t participate in a debt based economic model?

Credit bureaus are not infallible, and their data may contain errors or omissions, potentially leading to legitimate customers being denied access to their accounts due to incorrect or missing phone numbers.

This verification method raises privacy concerns, as it involves sharing personal information with a third-party credit bureau without the customer's explicit consent.

Banks should offer multiple verification options to accommodate diverse customer needs and ensure equal access to financial services.

Here are some Actions for Banking Customers to Pursue:

Escalate the issue with your bank and request that they reinstate traditional verification methods like security questions or recent transaction details.

If the bank refuses to provide alternative verification options, consider filing a complaint with the appropriate regulatory agency, such as the Consumer Financial Protection Bureau (CFPB) or the Office of the Comptroller of the Currency (OCC).

Advocate for inclusive and accessible verification practices that do not discriminate against individuals based on their access to technology or credit history.

Encourage your bank to adopt a multi-factor authentication approach that combines various verification methods, ensuring both security and accessibility for all customers.

It is crucial for financial institutions to strike a balance between fraud prevention and customer accessibility. Relying solely on a one-time text code from a credit bureau is an exclusionary practice that can deny legitimate account holders access to their funds, and banks should reevaluate this approach to ensure fair and equitable service for all customers

there are several drawbacks to using one-time codes (OTPs) for mobile banking identity verification:

Security Vulnerabilities

OTPs sent via SMS can be intercepted through SIM swap attacks, where attackers trick the mobile carrier into transferring the victim's phone number to a SIM card they control, allowing them to receive the OTP.

Phishing attacks can trick users into revealing their OTP to attackers who then use it to gain unauthorized access.

Brute force attacks can be used to guess OTPs, especially if they are short numeric codes.

Accessibility Issues

Relying solely on OTPs discriminates against individuals without mobile phones or those whose numbers are not registered with the bank or credit bureaus, denying them access to their accounts.

Elderly or low-income customers may not have consistent access to a mobile device capable of receiving OTPs.

Usability Challenges

OTPs can get out of sync with the authentication server, locking users out of their accounts if not submitted within a set timeframe.

If a user loses their mobile device or it gets stolen, they may be permanently locked out of their account until the issue is resolved with the bank, which can be inconvenient during travel or emergencies.

Costs for Banks

Implementing and maintaining OTP systems, especially hardware tokens, can be costly for banks compared to other authentication methods.

Providing customer support for OTP-related issues like lost devices or synchronization problems adds operational overhead.

While OTPs provide an additional layer of security beyond traditional passwords, their vulnerabilities, accessibility limitations, and usability challenges highlight the need for banks to offer alternative multi-factor authentication options or use OTPs in combination with other secure methods to ensure both security and inclusivity for all customers.

Jon Forrest Little walks into his bank and listen to their answer

Boots on the Ground Video Report

Keep in mind:

To buy a typical used car today (that runs) is $10,000 and that’s one with around 100,000 miles on it

I asked for $5,000

She is stating they only have $10,000 for the entire week.

This is serving a city of 2.7 Million people

To wait on a “cash shipment” is a week.

Guess I can’t buy a car

ATM’s Max hold $20,000 (so one ATM is better than 4 Branch Locations)

I was quoted a week lead time

If two people have an emergency (2 people need to fix their car) then all the other customers can’t have money

I've reached out to my friend Larisa Sprott, and together, we're determined to turn this true crime story into a real-life solution. Since this incident I have also noticed a growing number of people having trouble accessing their funds.

Larisa and I are going to be hitting the airwaves now with a series of strategies to counter the modern day banking problems

People are going to want:

1. Privacy

2. to become their own bank

3. Reduce dependency on banking that reports to IRS

4. Increase freedom from being tracked, fined, frozen, and spied on

-to be continued

-end of section

Banks do not have liquidity

The Secured Overnight Financing Rate (SOFR) is a key interest rate banks use when lending money to each other overnight.

SOFR jumps when there's increased demand for short-term loans - it seems banks need some cash on hand.

It could indicate that banks are kind of anxious, nervous.

They need more money on hand because they might sense upcoming problems with liquidity,

or even bank runs.

There are 63 banks on the FDIC Problem Bank List in 2024

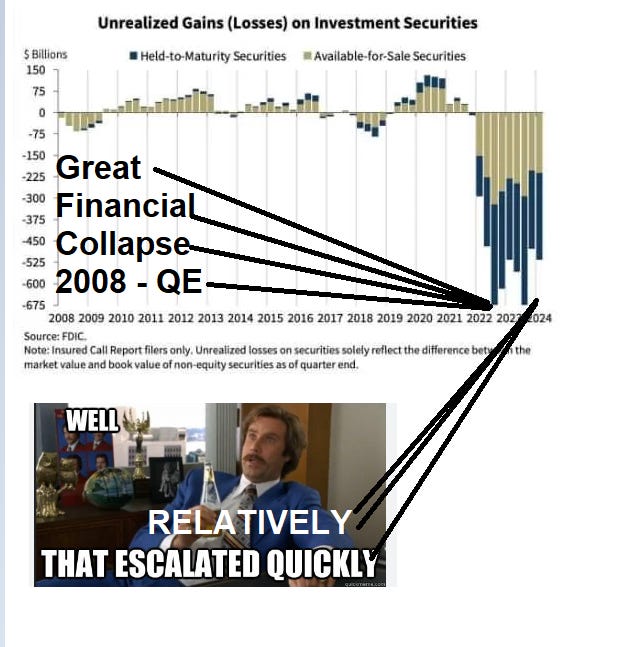

As we move through 2024, the U.S. banking system faces significant challenges, with reports indicating a staggering $517 billion in unrealized losses threatening the stability of 63 banks. This situation has brought the health of the entire system under intense scrutiny, raising concerns about potential insolvency and the broader implications for the economy.

https://www.fdic.gov/resources/resolutions/bank-failures/failed-bank-list/

The FDIC has indeed reported that 63 banks are on its "Problem Bank List" as of the first quarter of 2024.

Here are the key details:

Unrealized losses: The US banking system is facing $517 billion in unrealized losses, an increase of $39 billion from the previous quarter.

Problem Bank List: The number of banks on this list increased from 52 in Q4 2023 to 63 in Q1 2024.

Definition of problem banks: These are institutions with a CAMELS composite rating of '4' or '5', indicating financial, operational, or managerial weaknesses that could lead to insolvency.

Proportion of affected banks: The 63 problem banks represent 1.4% of total banks, which the FDIC notes is within the normal range of 1% to 2% for non-crisis periods.

Assets held: Problem banks hold $82.1 billion in total assets, an increase of $15.8 billion from the previous quarter.

Ongoing challenges: The FDIC warns that persistent inflation, volatile market rates, and geopolitical concerns continue to pressure the banking industry.

Areas of concern: The FDIC specifically mentions potential deterioration in office property and credit card loan portfolios as areas requiring continued monitoring.