It's Happening NOW and this system is working its Way to USA. Vietnam requires facial recognition for digital payments

It's Happening NOW and this system is working its Way to USA. Vietnam requires facial recognition for digital payments

Facial Recognition: It usually starts with the airports and drivers licenses then makes its way over to Banking.

Vietnam has implemented new regulations requiring facial recognition for digital transactions of 10 million dong ($390) or more, effective Monday.

This requirement applies to bank transfers and e-wallet payments, including purchases of high-value items like laptops or rent payments.

Under these new rules, customers must use facial recognition technology through their mobile banking apps to complete qualifying transactions.

The implementation of this biometric verification system comes as digital banking transfers are becoming increasingly common in Vietnam.

The introduction of facial recognition for financial transactions has raised concerns about privacy and security. As digital bank transfers continue to grow in popularity, the use of facial recognition technology for payments may become more widespread in Vietnam.

When The State (and the Bank) starts to clamp down with Authoritarian Measures and Controls Gold Soars

Gold (and Silver ) are the Counter Measures and Why we call it a SAFE HAVEN

Carl Menger, founder of the Austrian School of economics, was the first to explain that money is liquidity and that gold is the most liquid asset.

So when your bank says things like we have to install better KYC (know your customer) regulations or AML (anti money laundering) policies it is not true, they are not concerned about crime, they want to control their money and prevent bank runs.

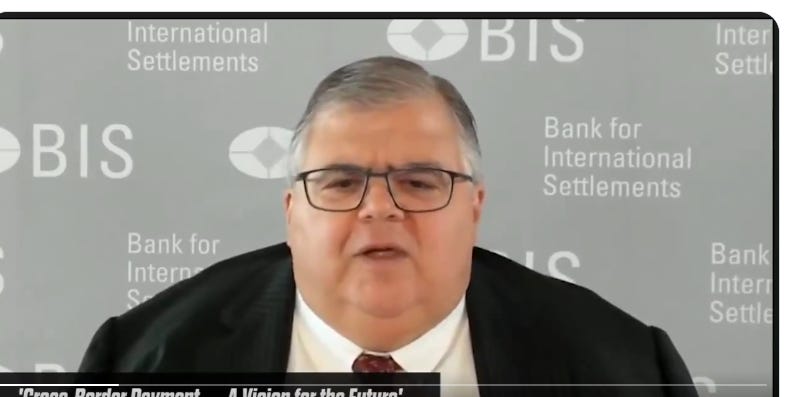

This is Agustin Carstens, the manager for the BIS (Bank for International Settlements), the bank that controls all other central banks.

“We don’t know, for example, who is using a 100 dollars bill today. We don’t know who is using a 1000 pesos bill today.”

He continues, “A key difference with the CBDC is that the Central Bank will have absolute control on the rules and regulations that will determine the use of that expression of Central Bank liability, and also we will have the technology to enforce that.” In other words, the Central Bank will decide when and how you are going to be able to spend YOUR own money, and they will have the technology to enforce that. If they don’t want you to spend the CBDCs on meat, gas, or air tickets your digital money will simply be denied at the time of purchase. And that is because it will be programmable. CBDC is intended for control, not stopping crime.

Getting the public to buy into a token or digital currency (on your phone) is a challenge. One way the Central Bankers will do this is inflict enough pain on the population through the inflation tax.

At this point there will be enough desperation in society that when forced with the alternative of starving to death the people will be coerced into accepting the terms of the CBDC and all its trappings:

1. Your movement is tracked on your phone.

2. Your transactions are recorded to see patterns in your buying habits.

3. Your taxes automatically deducted or fines can be instantly levied. (Encouraging obedience and compliancy with the Apparatus of the State)

4. Your funds expire.

5. Your funds frozen for dissent

Is this some off-kilter conspiracy theory? I think not!

I have a personal story to share with our readers. My bank funds were recently frozen and it took almost a month to recover. I will be getting into these details as soon as I come up with some courage to disclose how horrifying these events are.

I am 100% convinced that my personal story is going to be part of your future soon and that is why I am compelled to share this with you all (as soon as I organize my thoughts and test my thesis via social listening to see if other villagers are experiencing the same conditions )